Agenda 2012: State Tax Reform -- Corporate Income Tax | Eastern NC Now

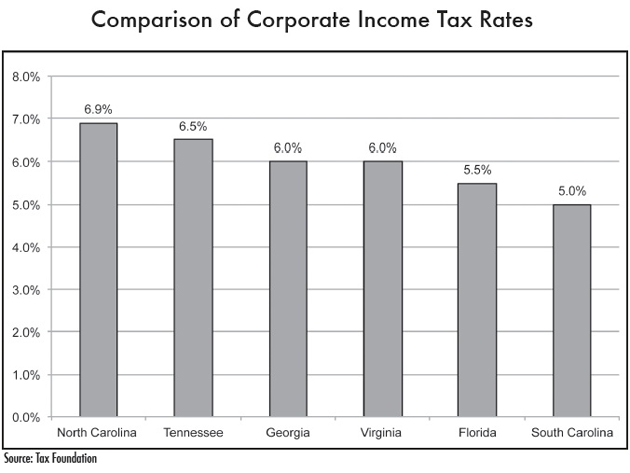

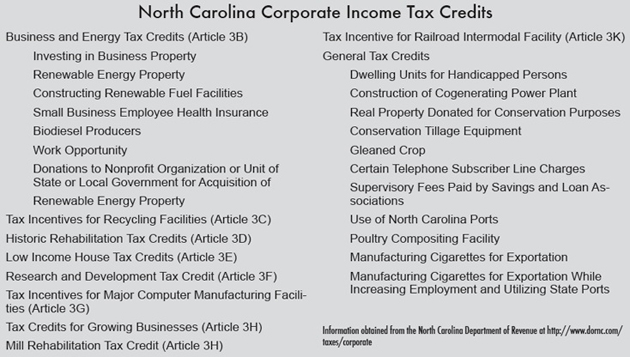

North Carolina's corporate income tax violates basic principles of sound economic policy and open government.

| Court Could Limit Appeal of Competitive Contracting | John Locke Foundation Guest Editorial, Editorials, Op-Ed & Politics | An Inescapable Fact about Poverty |

|

DSA tajeiover of Democrat Party is underway

Published: Wednesday, July 29th, 2026 @ 4:56 pm

By: John Steed

|

|

fortunately this travesty has not yet come to Beaufort County, but it has in Virginia

Published: Wednesday, July 29th, 2026 @ 12:19 pm

By: John Steed

|

|

now Fauci should be indicted for his previous lies under oath to Congress

Published: Wednesday, July 29th, 2026 @ 11:22 am

By: John Steed

|

|

Hochul's lead narrows to 4 points in heavily Democrat state

Published: Wednesday, July 29th, 2026 @ 8:48 am

By: John Steed

|

|

Biden was a figurehead for his handlers for all 4 years

Published: Tuesday, July 28th, 2026 @ 10:39 am

By: John Steed

|

|

Queen Garris has made a post on the Beaufort County GOP site that you should read. It is disloyal to conservative candiates key in the following: https://www.Facebook.Com/beaufortcountygop

Published: Tuesday, July 28th, 2026 @ 9:03 am

By: Hood Richardson

|

|

another reason we need the SAVE America Act that Democrat politicians fear

Published: Tuesday, July 28th, 2026 @ 9:00 am

By: John Steed

|

|

False narratives and autocratic behaviors continue.

|

|

Throughout the evening, the fireworks and other program events competed with uncooperative weather.

Published: Monday, July 27th, 2026 @ 7:40 pm

By: Daily Wire

|